2016 Survey of Connecticut Businesses

Now in its 15th year, CBIA and BlumShapiro’s Survey of Connecticut Businesses examines the near-term outlook, profitability, export activities, workforce trends, technology investments, and legislative priorities of Connecticut’s business community.

The 2016 Survey of Connecticut Businesses was distributed to top business executives from mid-June through early July, during a period of steady but slow economic growth; the state’s first reported monthly job losses for the year; and historically high voter disapproval of state leadership, according to a Quinnipiac University Poll.

The good news? These factors notwithstanding, most businesses this year are reporting profits and introducing new products and services.

The good news? These factors notwithstanding, most businesses this year are reporting profits and introducing new products and services.

There is, however, cause for concern. All the businesses surveyed have operations and/or headquarters in Connecticut, and 98% of manufacturers surveyed handle at least some of their production here, but fewer than half say they will continue to make job-creating investments in the state.

Key Findings

- Profitability among Connecticut companies is at a 10-year high: Roughly two-thirds of those surveyed (68%) showed a profit last year, a level not seen in our surveys since 2005.

- Only 47% say they will continue making job-creating investments in the state.

- Consistent with past surveys, new technology is the area of greatest investment (28% of this year’s respondents), followed by property/facilities, and employee training (both 24%).

- Businesses are nearly evenly split on the question of credit availability, with 51% saying it’s not a concern for them.

- A slight majority of companies (52%) introduced a new product or service in the past year, and more (55%) expect to in the coming year.

- The greatest barriers to growth, in order, are Connecticut’s costly government regulations, taxes, uncertainty surrounding legislative decision-making, and the state’s high cost of living.

The greatest barriers to growth are costly government regulations, taxes, and uncertainty surrounding legislative decision-making.

- More than a third of respondents report that state regulations are hampering their business, and 60% characterize those rules as complex and vague.

- Ninety percent feel elected officials do not understand their business and its challenges; fewer than one in 10 believe elected officials care about helping their business.

- Although most are not planning to relocate their business, half of our respondents say they are considering establishing residency outside the state to lower their personal tax burden.

- Most top executives surveyed (83%) are over age 50; of those, more than half are 61 or older.

- One in five respondents anticipates selling the business within the next five years. Another 18% plan to sell within 10 years, and 15% are undecided.

Business Growth, Innovation, and Investment

Business Growth, Innovation, and Investment

Business Growth, Innovation, and Investment

Business Growth, Innovation, and InvestmentMuch of the news regarding business growth from this year’s survey is positive. Three times more Connecticut companies are expanding than contracting. About half (51%) are holding steady. Nearly five times as many companies (68%) recorded a profit last year as those that recorded a loss (15%).

The single most important factor driving margins is sales.

Businesses are making their greatest investments in new technology (28%), followed by property and facilities and employee training (both at 24%). Other areas of investment are capital assets (16%) and research and development (8%).

Businesses are making their greatest investments in new technology (28%), followed by property and facilities and employee training (both at 24%). Other areas of investment are capital assets (16%) and research and development (8%).

Innovation is critically important in a high-cost state such as Connecticut, as new products and services often command premium prices.

More than half of all businesses surveyed (52%) introduced a new product or service over the past year, and 55% expect to in the coming year. This number trended upward over the last three years.

In 2015, 50% of businesses said they introduced a new product in the previous year, and 52% planned to in the coming year. In 2014, those figures were 46% and 47%, respectively.

Although Connecticut’s post-recession economic recovery trails that of the region and nation, the steady decline in the percentage of companies reporting losses and the increase in those that are profitable (as opposed to just breaking even) is encouraging.

Exporting

One-third of all respondents, including non-manufacturers, are exporting goods or services.

Among manufacturers surveyed, more than three-quarters (76%) are engaged in international trade.

Fifty-seven percent of exporters attribute at least 10% of their sales to exports. The biggest foreign market for Connecticut’s exporters today is North America (Canada/Mexico), followed by western Europe and northern Asia/Pacific Rim.

Top export destinations include:

- North America (88%)

- Western Europe (60%)

- Northern Asia/Pacific Rim: China/Japan/Taiwan/Korea (56%)

- South America (36%)

- Southern Asia: India/Indonesia/Malaysia (31%)

- Central America (26%)

- Eastern Europe, excluding Russia (35%)

- Australia/New Zealand/Pacific Islands (21%)

- Middle East (23%)

- Russia (13%)

- South Africa (11%)

Foreign markets identified as having the greatest potential for future exports are the same places where businesses currently export; however, fewer companies seem to see future potential there. For instance, only 30% identified China and Japan as their prime markets in the future; 22% identified western Europe as a prime market.

Foreign markets identified as having the greatest potential for future exports are the same places where businesses currently export; however, fewer companies seem to see future potential there. For instance, only 30% identified China and Japan as their prime markets in the future; 22% identified western Europe as a prime market.

Part of this has to do with the robust U.S. dollar, which continues to strengthen against most of the world’s major currencies.

While a strong dollar has its benefits for importers, major multinationals and smaller domestic exporters may struggle to sell their products overseas (because they are too expensive for foreign buyers) or take a hit when converting payment in foreign currencies back to U.S. dollars.

June 23 marked the historic European Union referendum—Brexit—in which British voters decided to withdraw from the EU.

(Although trade between Britain and the United States makes up only 0.5% of U.S. economic activity, the European Union is a major trade partner with the U.S., and concerns about other nations leaving the EU have created volatility in global stock markets.)

The day after Brexit was announced, the U.S. dollar rallied against the British pound for the biggest one-day gain since 1967.

The potential for diminished exporting activities can also be traced to some of the open-ended responses to our question, “What was the most important factor driving [your company’s] profit or loss?”

Answers included:

- Market collapse in commodities

- Offshore competition

- Scrambling to get work

- Poor sales results

- Low margins, high overhead

- Lost customers to Mexico

Challenges to Growth; Public Policy Implications

Despite what would otherwise be seen as positive indications of confidence, respondents overwhelmingly expressed apprehension over the volatile and unstable climate in state government.

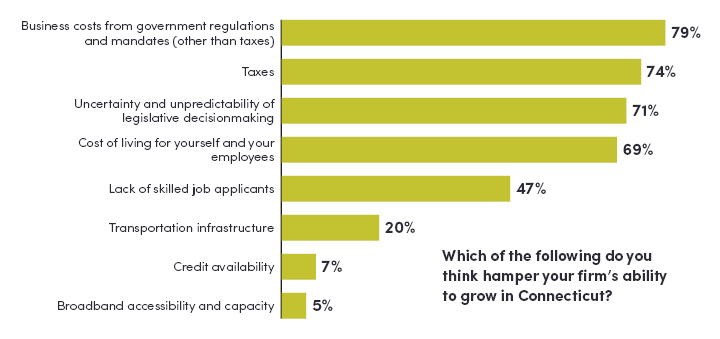

The cost associated with complying with state regulations is the number-one challenge for Connecticut businesses this year (79%); taxes are a close second (74%), followed by uncertainty or unpredictability surrounding legislative decision-making (71%) and the state’s high cost of living (69%).

Lack of skilled workers was identified as a challenge by nearly half of our respondents (47%), and those providing open-ended responses named healthcare costs, energy prices, and a weak economy as major hurdles.

Lack of skilled workers was identified as a challenge by nearly half of our respondents (47%), and those providing open-ended responses named healthcare costs, energy prices, and a weak economy as major hurdles.

Regarding their regulatory burden, 60% of businesses agreed with the statement, “State regulations are complex and vague, and making the effort to understand them costs time and money.”

More than a third (34%) said state regulations are hampering their business, while 27% agreed with the statement, “My organization complies with state regulations without difficulty.”

Only five percent agreed with the statement, “State regulatory agency staff has been easy to work with, understands my organization, and helps us comply with regulations in a cost-effective manner.”

Nine out of 10 respondents agreed with the statement, “I feel that elected officials do not understand my business and its problems.” Fewer than one in 10 (8%) believe elected officials “really care about helping my business.”

Nine out of 10 respondents agreed with the statement, “I feel that elected officials do not understand my business and its problems.” Fewer than one in 10 (8%) believe elected officials “really care about helping my business.”

In a positive development this legislative session, a bill addressing small business regulations was enacted after a veto by the governor was overruled.

The law is designed to minimize the adverse impacts of new regulations on small businesses by requiring state agencies to more rigorously evaluate proposed regulations before final approval.

The law puts Connecticut in line with competitor states Rhode Island and Massachusetts, where state agencies must identify specific potential impacts such as additional training, staffing, consulting, legal fees, record keeping, reporting, and auditing and declare the extent to which the agencies communicated with small businesses during regulatory development.

CBIA lobbied vigorously for this new business-friendly law, which goes into effect Oct. 1, 2016.

Location

One in three companies has been approached by other states about relocating their business. Of those, nine out of 10 are not planning on moving to the states doing the outreach.

However, in one of the most significant findings in this year’s report, surveyed (47%) agreed with this statement: “My firm will continue to make job-creating investments in Connecticut.”

A closer look at other questions sheds some light on this finding.

Nearly every manufacturer surveyed (98%) handles at least some of its production in Connecticut, although 21% also have production facilities in other states, and 18% handle at least some of their production outside the U.S.

Among non-manufacturers, 20% have operations outside of Connecticut, and 9% outside the country.

More than one in four businesses (26%) say their company is considering shifting significant production or operations to another state within the next five years, and 31% are looking to set up new operations outside the state.

More than one in four businesses (26%) say their company is considering shifting significant production or operations to another state within the next five years, and 31% are looking to set up new operations outside the state.

Reasons cited include lower operating costs and taxes in other states, Connecticut’s heavy regulatory burden, the need to follow high-net-worth individuals who have left the state, and what one respondent termed a “hostile attitude of state government to business.”

“Connecticut does not support businesses,” another respondent wrote.

About half (51%) are considering establishing residency outside the state to lower their personal tax burden.

While 46% of respondents do not anticipate a sale of their company within the next 10 years, 15% are undecided, and the rest expect to sell—some as soon as this year.

Transportation

More than two-thirds of respondents (69%) say car and rail transportation in Connecticut is outdated and inadequate.

Thirty-seven percent believe that high-speed tolls, as a way of raising funds to upgrade roads and bridges, offer the best solution.

Wages

The deep recession that began in late 2007 wiped out primarily high-wage jobs around the country. Nowhere is that truer than in Connecticut, which lost nearly 15,000 jobs in financial services.

The state has yet to recover 100% of the jobs lost in the recession, and job creation by young Connecticut companies has failed to return to pre-recession levels.

Making the strongest comeback have been lower-wage jobs in industries like food services, hospitality, and healthcare.

This is largely reflective of a national trend, where the 2.6 million jobs added in higher-wage industries post-recession fell short of the 3.6 million lost—and the two million low-wage jobs shed during the recession have been replaced by nearly double the number of low-paying jobs (3.8 million).

The concern here, says CBIA economist Pete Gioia, is that Connecticut—traditionally a high-income, high-tax state—could become only the latter if these trends continue.

The concern is that Connecticut—traditionally a high-income, high-tax state—could become only the latter if these trends continue.

Considering the ratio of managers to employees, the fact that six percent of businesses see the single greatest demand for new employees at the upper levels of the organization could signal either the kind of growth that requires high-level employees or the reality that in some companies a large percentage of management is nearing retirement.

With the nationwide push for a minimum wage of $15 an hour, we asked Connecticut businesses about the potential impact on their business.

More than half (53%) would invest in robotics or other alternatives to avoid expanding their workforce. Nearly one in four (24%) would consider closing or moving their operations.

Clearly, although many businesses pay their employees more than the minimum wage, aggressively mandated wage hikes could lead to job losses.

Workforce and Succession

Population trends—negligible growth, looming retirements, and high domestic out-migration—are reshaping Connecticut’s workforce.

On average, businesses surveyed anticipate losing 2.6% of their workforce to retirement this year. In 2017, the number increases to 3.6%.

Between 2018 and 2021, retirements are expected to claim 10% of current employees. In short, over the next five years, respondents will have to replace upwards of 16% of their current workers.

What makes this especially challenging is that three of the top six U.S. cities losing the highest percentage of their population to other states are located in Connecticut.

Many of the residents leaving are young, educated people.

Connecticut has the added problem of students finishing school here but seeing greater opportunities for jobs elsewhere.

Connecticut has the added problem of students finishing school here but seeing greater opportunities for jobs, recreation, and affordable housing elsewhere.

Open-ended responses describing what companies are doing to replace retiring workers ranged from “everything” to “nothing.”

Nearly half of the companies surveyed are hiring and training new workers, including apprentices. A number are cross-training and promoting existing workers, and a few are automating or outsourcing.

While many businesses are actively recruiting based on future needs (“hiring replacement workers when they are available, not when we need them”), a large number simply plan to downsize, consolidate, or transition to new business models.

Some are raising wages and benefits to attract and retain workers; others say they will not replace workers in this state.

Conclusion

Connecticut has long been one of the nation’s leaders in key categories that underpin a state’s economic competitiveness—the strength of its workforce, education system, base industries, and R&D.

Several trends, however, threaten to undercut these strengths. Chief among them is the state’s chronic fiscal instability, which shakes business confidence and inhibits job-creating investment.

While more businesses are profitable this year than at any time since the recession, fewer than half plan to make investments in this state.

Notable in this year’s survey is the fact that while more of Connecticut’s businesses are profitable this year than at any other time since the 2008 recession, fewer than half plan to make job-creating investments in this state.

The state’s regulatory burden, taxes, and uncertainty in legislative decision-making are high on the list of business challenges and will be high-priority items for CBIA in the upcoming elections and legislative session.

Methodology and Demographics

This year’s survey was mailed and emailed in June and July to 2,900 top executives throughout Connecticut; 331 participated in the survey, for a response rate of 11.4% and a margin of error of +/–5.5. Just over one-third of respondents (115) were manufacturers.

All figures are rounded to the nearest whole number and may not total 100%.

The largest share of participating companies are privately held (48%) and family-owned (41%). Business types also include S corporations (34%), incorporated (25%), LLC (13%), woman-owned (10%), veteran-owned (6%), publicly held (2%), minority-owned (2%), and foreign-owned (2%).

RELATED

EXPLORE BY CATEGORY

Stay Connected with CBIA News Digests

The latest news and information delivered directly to your inbox.

CBIA IS FIGHTING TO MAKE CONNECTICUT A TOP STATE FOR BUSINESS, JOBS, AND ECONOMIC GROWTH. A BETTER BUSINESS CLIMATE MEANS A BRIGHTER FUTURE FOR EVERYONE.