State-Run Healthcare’s Costly Price Tag: Who Pays?

Lawmakers this week introduced legislation implementing a state-run healthcare plan that would drastically alter Connecticut’s health insurance landscape.

The legislature’s Insurance and Real Estate Committee is planning a Feb. 9 public hearing on the controversial measure, SB 842.

The first part of the bill authorizes state Comptroller Kevin Lembo to offer health insurance coverage to multi-employer plans and businesses with less than fifty employees and nonprofit employers, and pool these lives with state workers and retirees under the state employee plan.

Premiums would be adjusted to reflect age, geographic area and family size, but cannot be adjusted more than 3% each year.

Deductibles would also be capped at the IRS minimum and coverage must be approved by the Office of the State Comptroller’s Cost Containment Committee during a public meeting.

Additionally, multi-employer plans and nonprofit employers would be required to hold coverage for three years, while small businesses would be required to hold coverage for one year.

In previous iterations of this bill, small businesses were required to hold coverage for a minimum of three years.

Small Business Burden

The public option proposal also allows the Comptroller to establish a risk fund to pay claims that exceed the premiums collected in a given plan and would levy charges against small employers, nonprofits, and multiemployer plans to adequately fund it.

If implemented, this then leaves small businesses as the financial backstop against any future deficits the public option plan may encounter.

Of the 231 small business members that CBIA polled last month concerning a public option plan, 63% expressed opposition.

Fifty-seven percent said they were concerned that taxpayers would subsidize plan deficits and almost 50% said they don’t trust the state to manage health insurance plans.

These concerns are well-warranted given the state’s inability to administer a solvent municipal partnership plan for the past few years.

That plan lost $31.9 million in 2019, tripling its losses from the previous year.

Connecticut taxpayers were the backstop to subsidize those losses then, and if a risk fund is created under this proposal, small businesses who opt-in to the plan will be the backstop in the future.

Higher Premiums?

Small businesses are also concerned about the potential for the plan to destabilize the private marketplace and lead to higher premiums for owners and their employees.

If low-risk, low-cost employees flood this new program, the private marketplace will be disproportionately burdened with a high-risk pool and premiums will rise across the board.

This plan also would not be subject to Connecticut Insurance Department regulations and allows the Comptroller’s office great flexibility to suppress premiums and offer benefit-rich packages without fear of the plan being discontinued.

Small businesses are concerned the plan will lead to higher premiums for employers and their employees.

This is contrary to the rules that private insurers offering coverage for small employers have to follow.

For these insurers, $0.80 in claims on every $1 of premium they collect must pay out claims with the remainder going to administrative costs.

This uneven playing field will create an unfair landscape for competition and cause financial distress and job losses for one of Connecticut’s main economic drivers.

New Assessments

The second part of the bill authorizes the Office of Health Strategy to levy up to $50 million annually in new assessments to carry out health exchange changes after seeking a 1332 State Innovation Waiver from the federal government.

The money derived from this new assessment would be deposited into a new general fund account: the Connecticut Health Insurance Exchange.

The bill levies the assessment against each insurer and healthcare center doing business in the state, as well as insurers that administer self-insured health benefit plans.

Employers are shifting to self-insured plans because they are subject to federal, not state, regulations and can save consumers up to 25% annually.

As of 2019, 65% of employer health plans are self-insured and 35% are fully insured.

Employers shifted to self-insured plans in recent years because they are subject to federal, not state, regulations and thus can save consumers up to 25% annually.

For plan year 2022 and subsequent plan years, OHS, with consultation from the exchange, can use funds from this new account to (1) reduce the cost of qualified health plans for persons with a household income less than 200% of the federal poverty level by, among other things eliminating premiums; (2) make coverage more affordable for persons who are ineligible for coverage under a QHP by, among other things, providing premium and cost-sharing subsidies (not exceeding $25 million).

Health Insurance Tax

With the federal Health Insurance Tax repealed by Congress last year, insurance premiums were lowered this year as a result.

If OHS assesses fully-insured and self-insured plans under this bill, premiums will rise again across the board.

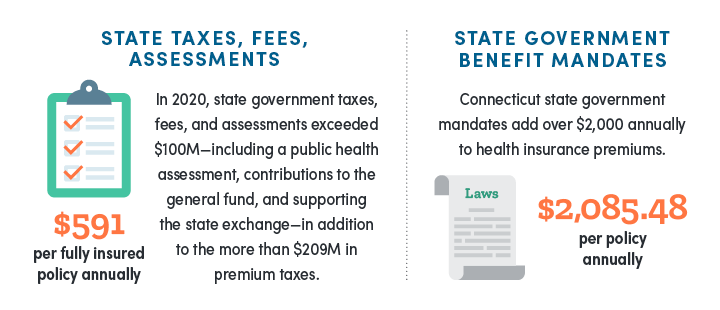

State-imposed fees and assessments continue to be a major healthcare cost driver, adding about $591 to the annual premium costs in the fully insured market.

If OHS assesses fully-insured and self-insured plans, premiums will rise again across the board.

The latter part of the bill deals with reforms to the Medicaid for Employees with Disabilities (Med-Connect) program and general Medicaid eligibility.

Seeking to expand disabled worker access to Med-Connect, the bill removes the restriction that claimants must have less than $10,000 in assets.

The bill also increases the qualifying threshold for Husky A (parents and caregivers) from not more than 155% of the FPL to not more than 201%.

For more information, contact CBIA’s Wyatt Bosworth (860.244.1155) | @WyattBosworthCT

RELATED

EXPLORE BY CATEGORY

Stay Connected with CBIA News Digests

The latest news and information delivered directly to your inbox.

CBIA IS FIGHTING TO MAKE CONNECTICUT A TOP STATE FOR BUSINESS, JOBS, AND ECONOMIC GROWTH. A BETTER BUSINESS CLIMATE MEANS A BRIGHTER FUTURE FOR EVERYONE.