Lack of Spending Controls Feeds Deficit, Tax Hike Cycle

The message Connecticut voters delivered to lawmakers 25 years ago was clear—if you’re going to impose a state income tax, something must be done to control state government spending.

That’s why voters, by an 81% margin, in 1992 approved a constitutional spending cap the year after adoption of the state income tax.

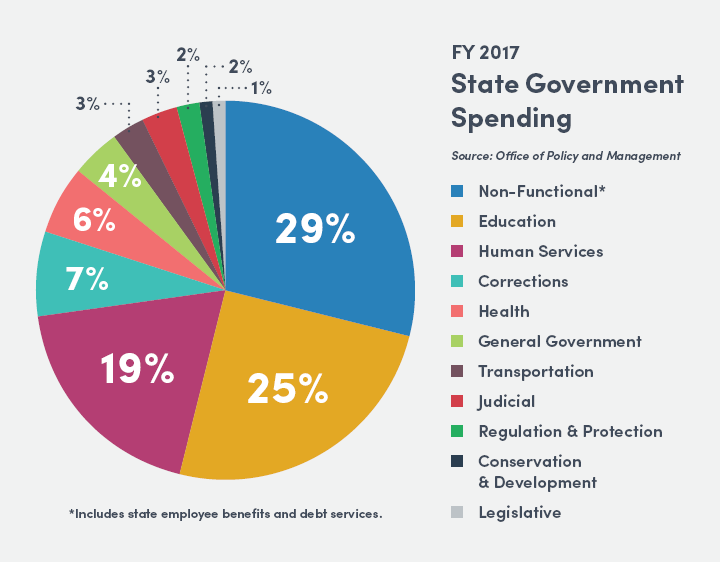

State government spending is expected to total $19.7 billion this fiscal year.

Lawmakers continued to find new ways to exclude spending from the cap, leading to massive budget deficits and the adoption of two of the largest tax increases in state history in 2011 and 2015.

As lawmakers struggle to draft a two-year budget for the fiscal years beginning July 1, 2017, the state is again facing a huge deficit—$3.6 billion over the next two years.

CBIA’s Brian Flaherty and Peter Gioia testified April 3 before the General Assembly’s Appropriations Committee in favor of HB 6511, designed to put some bite into the spending cap.

It’s one of several spending cap bills from lawmakers on both sides of the aisle.

“The definition of what is included under the cap has shifted over time as more and more spending has been removed from under it,” said Flaherty, CBIA’s senior vice president for public policy.

“It’s made the cap less effective and less able to encourage the fiscal stability it was written for.”

The State Spending Cap Commission worked for almost a year in 2016 but failed to reach a consensus on how to fully enforce the cap.

Gioia said a working spending cap is critical to CBIA members and all businesses.

‘Sustainability Encourages Investment’

“Our members need to have faith that the General Assembly policymakers will have consistency and predictability in producing a budget within our means,” said Gioia, CBIA’s economist.

“Predictability and sustainability in state spending will encourage economic investment, and increase business confidence and job creation.

“We can achieve this with a spending cap that is as comprehensive as envisioned by the original constitutional amendment.”

A proposal from Gov. Dannel Malloy places a cap on general fund expenditures but exempts debt service and unfunded liabilities in the state’s pension system.

Gioia said the language of the 1992 spending cap may not specifically address unfunded pension liabilities, but noted the bill’s authors certainly intended them to fall under the cap.

“They wanted the General Assembly to deal with it before it became a crisis,” he said.

“The reason unfunded liability was not included in the cap when it was first adopted was to keep pressure on lawmakers to reform the pension system,” Flaherty added.

There’s plenty of talk about the potential for more tax hikes to balance the budget. It’s the last thing Connecticut’s economy needs.

Appropriations Committee ranking member Rep. Melissa Ziobron (R-East Haddam) agreed that unfunded liabilities should be included under the cap. She is among several lawmakers who supported a bill to count unfunded liabilities against the cap.

“The 1992 mandate was clear and the situation is not simple,” Flaherty said. “Business owners are looking for a sign this legislature will honor the mandate of voters.”

Flaherty said there’s plenty of talk at the Capitol on the potential for more tax hikes to balance the budget.

It’s the last thing Connecticut’s economy needs.

“Our members want a sign that spending will be controlled. The best way is a strong, workable spending cap,” he said.

Flaherty said that while CBIA wants lawmakers to adopt a working spending cap, “we intend to work with this committee on long-term structural spending reforms.”

CBIA has long championed a working spending cap. In fact, enacting the state’s original spending cap is among the measures CBIA called for in its 2017 legislative and regulatory agenda.

Unfunded Mandates

Gioia and Flaherty also testified in favor of HB 5220, which requires a two-thirds vote of each legislative chamber to pass any law that imposes unfunded mandates on cities and towns.

“We feel the two-thirds vote effectively precludes any mandate unless it’s absolutely essential without prohibiting some future action, which may be essential,” he said.

For more information, contact CBIA’s Pete Gioia (860.244.1945) | @CTEconomist

RELATED

EXPLORE BY CATEGORY

Stay Connected with CBIA News Digests

The latest news and information delivered directly to your inbox.

CBIA IS FIGHTING TO MAKE CONNECTICUT A TOP STATE FOR BUSINESS, JOBS, AND ECONOMIC GROWTH. A BETTER BUSINESS CLIMATE MEANS A BRIGHTER FUTURE FOR EVERYONE.