The Amazing (Ta)X-Factors Driving Connecticut’s Economy

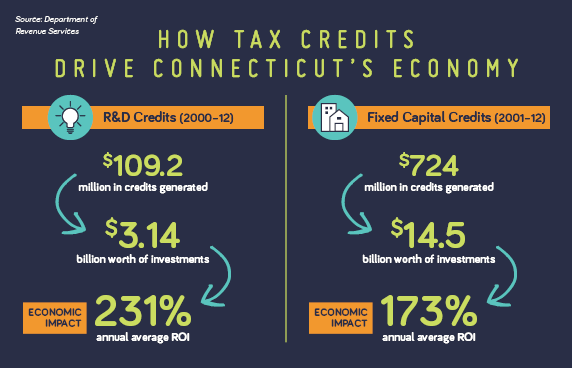

Should state policymakers jump at the chance for a proven, 231% average annual return on investment as a vehicle for driving Connecticut’s economy and tax revenues?

And should they pursue a strategy capable of producing $14.5 billion in direct investments in the state in a little over a decade?

Well, that’s exactly what lawmakers did years ago when they approved the state’s research and development (R&D) tax credit, fixed capital tax credits, and other strategies.

R&D tax credit: Transformed $109 million in tax credits into $3.14 billion in investments in Connecticut from 2000-2012, for an average annual ROI of 231%.

Fixed capital tax credit: Generated an average annual ROI of 173% per year from 2001-2012, producing $14.5 billion in Connecticut investments from $724 million in tax credits.

This week, however, the Finance Committee held a public hearing on proposals to weaken those credits and imperil the very economic activity they generate and which Connecticut counts on.

State lawmakers have to create a new two-year state budget that will keep Connecticut’s economy on the upswing and solve a billion-dollar-plus deficit.

But the Finance Committee this week explored proposals contained in SB 946 that actually would slow our economy down by:

- Reducing the use of earned investment incentives for research and development (R&D) , capital purchases, and other key economic drivers

- Limiting the use of the net operating loss carryforward that’s critical to growing investments in Connecticut

- Making permanent the 20% corporate surcharge that was scheduled to be eliminated this year

- Continuing the credit reduction for the insurance tax that was scheduled to be eliminated this year

As CBIA testified to the committee, these would be shortsighted and self-defeating changes.

For many years, strategic state tax policy has produced an amazing ROI that’s propelled our economy, created jobs, and fueled tax revenues–supporting and growing new and bedrock job creators, in industries including biopharma, financial services, defense, and manufacturing.

What Are Tax Credits?

Tax credits are revenue-generating incentives that lawmakers have adopted to encourage companies to make certain investments in this state.

The rules are fair but tough: Only investments made in Connecticut can earn tax credits. There is no cost to the state until after a Connecticut investment is made, and in fact, the revenues generated as a result of the investment far exceed the credit earned.

Why Tax Credits Matter

Investment incentives matter greatly to Connecticut because they enable the state to be competitive. The availability of credits is often a significant factor in the decisions made by job creators on where they will locate.

And credits are an important tool for offsetting costs where Connecticut is not competitive. Nearly all state and foreign jurisdictions offer credits, and only three states have permanent limitations on the use of credits.

Tax Increase

If lawmakers were to limit these credits, it simply would raise taxes strictly on Connecticut companies–not those companies that use the state as a market but don’t have a physical presence here.

What’s more, these proposals would retroactively increase taxes on the very job creators that have already made the investments that Connecticut lawmakers have asked them to make.

Net Operating Losses

Start-up businesses, new product development, and economic downturns are three most common reasons for the use of net operating loss (NOL) carryforwards as an important mechanism for attracting and keeping long-term investment in a state.

NOL carryforwards allow companies to either offset losses in the year they’re incurred or in a future year. This allows companies that are developing products, or those that are struggling, to overcome a mismatch between a business cycle and a tax year.

Why NOLs Matter

Connecticut has to remain competitive. All states with an income tax allow NOLs, and only two states have permanent limitations on NOL carryforwards.

Any limitation will make Connecticut much less attractive for businesses with significant upfront investments—such as startups—and therefore will weaken our economic competitiveness.

Permanent Rate Surcharge

Only five states have a higher corporate business tax rate than Connecticut’s. The tax rate was set at 7.5% years ago in an attempt to make Connecticut more competitive, but the proposal before the committee would make a current surcharge permanent and bring the business tax rate to an uncompetitive 9%.

Elimination of the Business Entity Tax

The Business Entity Tax (BET) has been a nuisance tax since its creation. It’s not based on revenues but is simply a tax for a business being in business. CBIA supports elimination of the BET.

Consistency, clarity, and fairness in state tax policy are achievable and critically important goals.

CBIA encourages the committee to reject the increased revenue proposals, eliminate the Business Entity Tax and encourage the Appropriations Committee to develop a budget that reduces costs and improves outcomes by adopting the recommendation of the Connecticut Institute for the 21st Century.

For more information, contact CBIA’s Bonnie Stewart at 860.244.1925 | [email protected] | @CBIAbonnie

RELATED

EXPLORE BY CATEGORY

Stay Connected with CBIA News Digests

The latest news and information delivered directly to your inbox.

CBIA IS FIGHTING TO MAKE CONNECTICUT A TOP STATE FOR BUSINESS, JOBS, AND ECONOMIC GROWTH. A BETTER BUSINESS CLIMATE MEANS A BRIGHTER FUTURE FOR EVERYONE.