Report Questions State-Run Healthcare Plan’s Viability

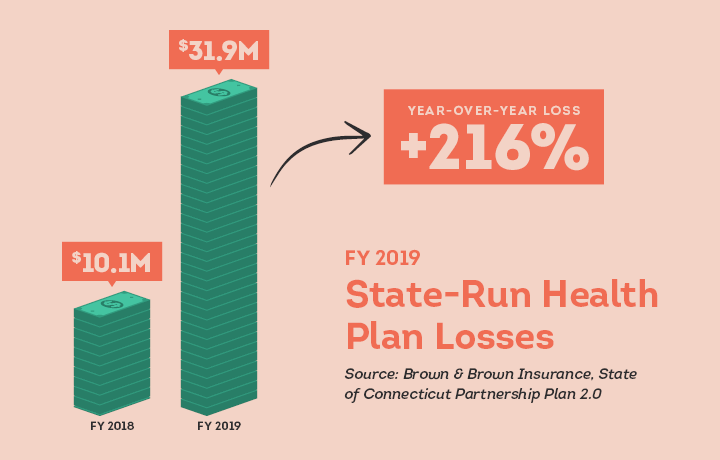

Connecticut’s state-run health plan for cities and towns lost $31.9 million in fiscal 2019—more than triple the $10.1 million in losses recorded the previous year.

An independent study by insurance brokerage Brown & Brown Insurance found the plan’s 2019 medical loss ratio was 108.4%, up from 105.2% in 2018.

This ratio is used to assess the fiscal viability of a healthcare plan, comparing claims paid to premiums collected.

The Connecticut Insurance Department requires private sector insurance plans to have a MLR under 100%.

The Brown & Brown study says state plan premiums would have to increase 17.3% to cover projected costs, compared with the average 9.2% annual increase for private sector plans in the small group market.

However, Brown & Brown estimates the plan has a current $47 million shortfall, requiring a 26.7% premium increase to cover costs and runout claims.

“The [plan’s] overall trend has been climbing slightly faster than the renewal increases being issued by the state,” the report said.

“That raises some concerns regarding the adequacy of the premiums being collected versus the claims being paid.”

Plan Expansion Bill

The Office of the State Comptroller administers the State Partnership Plan 2.0, which covers approximately 23,100 town, city, and other public sector employees.

The state charges municipalities over $10,000 per enrolled employee annually to participate in the plan.

“That raises concerns regarding the adequacy of the premiums being collected versus the claims being paid.”

Brown & Brown Report

State Comptroller Kevin Lembo testified March 5 before the legislature’s Insurance and Real Estate Committee in support of legislation expanding the plan to small businesses.

SB 346 contains almost identical language to two bills that failed last session and allows small employers to purchase coverage for employees through state partnership plan.

‘Significant Solvency Issues’

CBIA president and CEO Joe Brennan told the committee hearing there were broad concerns about expanding the plan.

“It is unclear how small businesses will be affected if they enroll in a plan with significant solvency issues,” Brennan said.

“Small businesses are not in a position to subsidize the state’s health plan.”

CBIA’s Joe Brennan

“A public health program will already have significant cost implications for the state, but the plan’s cost-sharing subsidies create an even greater burden on Connecticut’s uncertain long-term financial stability.

“Additionally, the bill does not provide whether participants or taxpayers will be responsible for funding the plan.”

Cost Drivers

Brennan said that while employers appreciate efforts by policymakers to reduce healthcare costs, small businesses are not in a position to subsidize the state’s health plan.

“Looking for innovative ways to expand access to health insurance should be encouraged,” he said.

“However, creating a buy-in to the state employee plan for small businesses will destabilize the health insurance market, require taxpayer subsidies to finance the program, and do little or nothing to reduce healthcare or premium costs—the biggest barriers to acquiring health insurance.”

Brennan said policymakers should address the impact of state government assessments, taxes, and mandates—which add over $2,200 annually per premium—and the cost of care.

The Insurance and Real Estate Committee narrowly approved SB 346 on a 10-9 vote March 10, with Democratic senators Steve Cassano (D-Manchester) and Joan Hartley (D-Waterbury) joining all Republicans except Rep. Tom Delnicki (R-South Windsor) in opposing the bill.

For more information, contact CBIA’s Michelle Rakebrand (203.592.7532) | @MRakebrand

RELATED

EXPLORE BY CATEGORY

Stay Connected with CBIA News Digests

The latest news and information delivered directly to your inbox.

CBIA IS FIGHTING TO MAKE CONNECTICUT A TOP STATE FOR BUSINESS, JOBS, AND ECONOMIC GROWTH. A BETTER BUSINESS CLIMATE MEANS A BRIGHTER FUTURE FOR EVERYONE.