Economic Outlook: ‘Headwinds for Foreseeable Future’

McKinsey & Company’s Ezra Greenberg has no doubt as to the key factor influencing the economies of Connecticut and the rest of the nation.

“COVID is still with us, but many other risks are on the forefront of the minds of executives,” he told 250 Connecticut business leaders at CBIA’s Jan. 21 Economic Summit + Outlook.

He compared the shock of the initial pandemic restrictions to that of banging a gong: “We can’t get back to normal until the gong stops vibrating, and as far as I can tell the gong is still vibrating.”

Greenberg, a partner at McKinsey, has been at the center of the firm’s global response to the COVID-19 crisis.

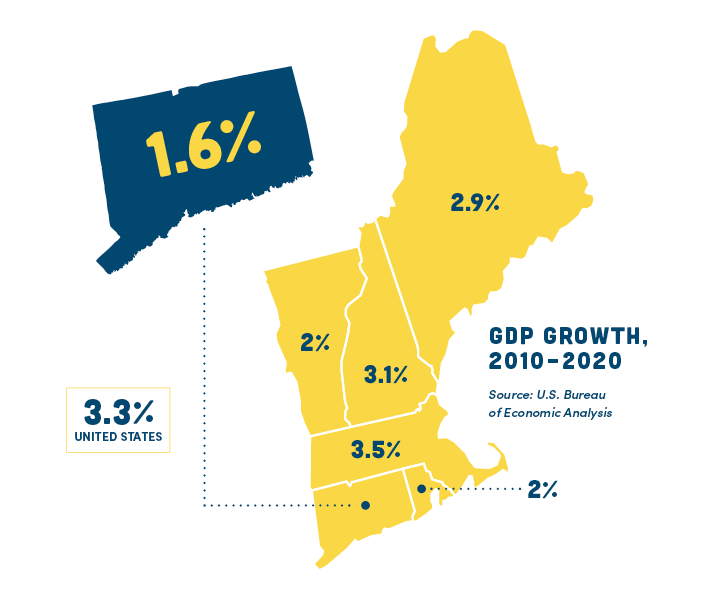

His outlook for Connecticut was mixed, noting that the state is making slow but steady progress, but “has responded slower than the national economy, and is facing some headwinds in the foreseeable future.”

He added that while Connecticut’s near-term fiscal health was strong, long-term concerns remain over the size of the state’s unfunded pension liabilities.

Financial Services ‘Uncertainty’

Greenberg also pointed to uncertainty around the financial services sector, long a mainstay of the state’s economy.

“Financial services has been a great thing for the state of Connecticut and there is some question about whether that’s going to be the source of growth going forward or whether we have to diversify,” he said.

There are, however, reasons for optimism.

“There’s a lot of pent-up demand and there’s real opportunities for productivity enhancement.”

McKinsey’s Ezra Greenberg

Greenberg highlighted the state’s high vaccination rates and the $5.4 billion in federal funds that will be invested in infrastructure programs across the state over the next five years.

“I do believe there’s a lot of pent-up demand, and I do believe that there’s real opportunities for productivity enhancement,” he said.

The transportation and warehousing sector also represents an area of growth Greenberg said, adding the state was “well-positioned” given its geographical advantages.

Jobs Recovery

Greenberg addressed factors influencing the state’s jobs recovery, which trails most of the region and country, compounded by a declining labor force and high unemployment.

Connecticut’s labor force participation rate and employment-to-population ratio remain below pre-pandemic levels and “bigger than the national drop-offs that we’ve seen.”

“This is actually what’s created a lot of the supply-demand imbalances, the labor mismatches, that we’re seeing in the economy,” Greenberg said.

“The question isn’t why we are seeing this, it’s why did we think it would be resolved quickly. Labor markets don’t respond quickly to these types of shocks.

“I like to say the labor market is like the supply chain with feelings. It takes a while for this to get sorted out. My guess is that it’s going to take another year.”

Labor Shortage

Greenberg said the labor shortage was a national issue, with a “skyrocketing” gap between job openings and available candidates.

“People are looking for something different and have been for some time,” he said. “The pandemic just massively accelerated that trend.”

“The question is: ‘Is that a new normal?’ Or is this something that is temporary?”

“People are looking for something different and have been for some time.”

Greenberg

Greenberg noted that higher wages—and subsequent inflationary pressures—were the result of the labor shortage, particularly in “high-stress industries.”

While Connecticut has only recovered 75% of its COVID job losses, Greenberg said the state was not feeling national wage pressures.

“Although there’s a lot of job openings, that has not translated to the type of wage pressure seen in other parts of the country,” he said.

Growth Struggles

CBIA president and CEO Chris DiPentima asked why Connecticut’s job and economic recovery trailed much of the region and the country, despite its position as a leader in navigating the pandemic.

Greenberg explained that “Connecticut has been growing in recent years less than the national average, and that’s caught up with us coming out of the recession.”

“There’s not as much dynamism or sector diversification in Connecticut as some other states,” he said.

Greenberg also warned “not to underestimate” the impact of federal pandemic relief funds “keeping us above water.”

Supply Chain Challenges

At the national level, Greenberg highlighted the contradictions between the perception and realities with supply chain issues.

He said that while many think the supply chain “is falling apart,” goods spending is 18% higher than expected.

Businesses “actually did an amazing job,” he said, “and it’s incredible they were able to deliver what they delivered.”

A McKinsey survey of supply chain executives revealed that increasing inventory and dual sourcing were the most commonly used actions by executives to combat supply chain and inflationary issues.

DiPentima asked Greenberg how long he expected supply chain bottlenecks to continue—”is this a 12-month issue or a three to five year issue?”

“Our sense is this is more a one-year issue than a long-term structural shift,” Greenberg replied.

Inflation

Greenberg said while the rapid increase in the inflation rate was largely in the past, “we are going to be at a higher level of inflation for the next couple of years.”

He projected a 3%-4% increase in inflation in 2022 and closer to 3% in 2023.

Greenberg expects that “we are going to be at a higher level of inflation for the next couple of years.”

He explained that the Federal Reserve is currently working to convince bond markets that inflation is under control.

The balance being made now is “keeping the markets and inflation expectations in line” while also “not taking the punchbowl away from the economy.”

“This navigation of how the Fed will get us from higher levels of inflation to something we’re more comfortable with is the thing to be watched in 2022,” he said.

The 2022 Economic Summit + Outlook was made possible through the generous support of Webster Bank.

RELATED

EXPLORE BY CATEGORY

Stay Connected with CBIA News Digests

The latest news and information delivered directly to your inbox.

CBIA IS FIGHTING TO MAKE CONNECTICUT A TOP STATE FOR BUSINESS, JOBS, AND ECONOMIC GROWTH. A BETTER BUSINESS CLIMATE MEANS A BRIGHTER FUTURE FOR EVERYONE.