2015 Hartford-New Haven-Springfield Business Survey

Together, the Greater Hartford, New Haven, and Springfield metropolitan areas represent one of the highest-potential business centers in the nation.

Comprising Hartford, Tolland, New Haven, and Middlesex counties in Connecticut, and Franklin, Hampden, and Hampshire counties in Massachusetts, the area is the second largest population, education, and economic center in New England.

Comprising Hartford, Tolland, New Haven, and Middlesex counties in Connecticut, and Franklin, Hampden, and Hampshire counties in Massachusetts, the area is the second largest population, education, and economic center in New England.

Home to 41 colleges and universities and 64,000 businesses, the region consistently ranks among the nation’s top 10 in advanced degrees, science and engineering doctorates, and new patents registered per capita.

Areas of excellence and investment include financial services, bioscience, aerospace, healthcare, education, insurance, precision manufacturing, research, and energy.

In addition to these assets and its close proximity to Boston and New York’s commerce, sports, and entertainment centers, the Hartford-New Haven-Springfield region also has the advantage of being a large and concentrated market, giving it a sizeable potential labor pool and ready access to consumers. It is the 20th biggest metro region in the U.S., ranking ahead of Denver and St. Louis, with twice the population density of those areas.

Since 2007, the New England Knowledge Corridor, the area’s primary driver for economic development and competitiveness, has partnered with the Connecticut Business & Industry Association to survey companies throughout the region about their priorities and challenges, including workforce development, transportation, international trade, and business costs.

Surveys are conducted every two years.

Key findings in 2015:

- Taxes are the greatest challenge to operating a business in the Hartford-New Haven-Springfield region.

- Respondents’ economic outlook shows improvement. While a weak economy and decreased consumer spending were identified as the primary challenge for nearly half of the respondents in the last two surveys (47% of respondents in 2013, and 46% in 2011), just over a quarter (26%) see this as their primary challenge today, and only 13% believe it will be their main challenge five years from now.

- As the economy improves, the percentage of businesses recording a profit is inching up: 62% were profitable in 2014, compared to 59% in 2012 and 54% in 2010. The percentage of businesses reporting a loss (16% in 2014) is up slightly from the previous survey (13% in 2012) but still down significantly from 2010, when one in four respondents were in the red.

- Businesses are nearly evenly divided about the region’s near-term economic forecast: 31% of respondents anticipate improved conditions in 2015, 32% expect some decline, and 37% believe conditions will remain stable.

- About a third of respondents have operations in both Connecticut and Massachusetts, and more expect to in five years. Nearly one in three companies surveyed said discrepancies and costs associated with licensing, taxes, regulations, and other factors are barriers to doing business across state lines.

Regional Assets & Challenges

Our surveys traditionally bear out that the greatest benefit to running a business in the Hartford-New Haven-Springfield region is the area’s quality of life.

However, while 35% of respondents in 2015 cited quality of life as the region’s greatest advantage, that represents a steady decline from 40% in our last survey, 43% in 2011, and 47% in 2009.

Proximity to customers (ranked first by 24% of respondents) and access to major markets (17% of respondents) are also seen as regional assets.

Sixty-three percent of respondents characterize the region’s cultural attractions as excellent or good, and 73% say the same about the region’s retail offerings.

Although 13% of businesses surveyed identified skilled workforce as the number-one advantage to doing business here, a shortage of skilled workers was also cited as the third biggest barrier preventing companies here from expanding.

In fact, nearly one in four respondents (23%) expects the skilled workforce shortage to become the single greatest challenge to operating a business here over the next five years.

The region’s top challenges in 2015 are:

- Taxes (31% of respondents)

- Weak consumer spending (26%)

- Labor shortage (18%)

- Regulatory climate (10%)

- Transportation infrastructure (6%)

Projected top challenges for 2020:

- Taxes (36%)

- Labor shortage (23%)

- Weak consumer spending (13%)

- Regulatory climate (10%)

- Transportation infrastructure (9%)

Economic Outlook

The percentage of Hartford-New Haven-Springfield businesses turning a profit is the highest it has been since the recession hit, with 62% recording a profit in 2014 and 67% expecting to in 2015. (In 2006, 65% recorded a profit, and 71% expected to in 2007.)

While businesses surveyed this year are split on whether economic conditions in the region will improve, decline, or remain stable, they are more optimistic about their own companies’ prospects, with 47% expecting more robust performance in 2015, and only 16% expecting performance to deteriorate.

Confidence in the U.S. economy is strongest, with 55% of respondents expecting improvement this year.

International Trade

For the vast majority of businesses surveyed, customers within the U.S. account for most of their sales revenue. Eighty-nine percent of the region’s businesses surveyed attribute more than 75% of their current sales to domestic clients.

Slightly fewer, however—83%—expect that to be the case five years down the road, when international sales represent a bigger slice of the pie.

One in ten businesses surveyed anticipates that by 2020, foreign markets will account for more than 25% of their sales.

Expansion

By 2020, 41% of respondents expect to have a presence in both Connecticut and Massachusetts. Today, 31% have operations in both states.

There are barriers, however, to conducting business across the Massachusetts–Connecticut state line, including differences in the two states’ licensing requirements, costs associated with maintaining licenses in both states, regulatory discrepancies/compliance issues, legal restrictions on franchises, different taxes and exemptions impacting certain transactions, unemployment insurance, and more.

If we are to promote regional business growth, economic activity, and job creation, this is an area that deserves further investigation.

Strategies for Growth

In 2009, 56% of Hartford-New Haven-Springfield businesses surveyed had no plans to expand their business—not a surprising result, given economic conditions at the time.

This year’s survey tells a different story. Only 10% of businesses do not plan to expand. The rest plan to deploy a number of strategies to grow their market and their bottom line. These include:

- Web-based marketing (42%)

- Direct mail (41%)

- Hiring additional workers (39%—a considerable decrease from 59% in 2013)

- Strategic alliances (36%)

- Investments in new technologies (35%)

- Employee training (34%)

- Investing in equipment (31%)

- Mergers/acquisitions (19%)

- R&D (12%)

Barriers to Growth

What makes it difficult for the region’s businesses to expand?

Different factors have become more—or less—significant over the last two years. Consumer spending has picked up and economic uncertainties have eased somewhat, for example, while concerns about the workforce shortage have intensified.

Compare the top seven answers today versus 2013:

Barriers to Growth, 2015

- Cost of doing business (52%)

- Economic uncertainties (47%)

- Shortage of qualified workers (30%)

- Affordable Care Act (23%)

- Domestic cost competition (21%)

- Decreased consumer spending (20%)

- Credit availability (13%)

Barriers to Growth, 2013

- Economic uncertainties (61%)

- Cost of doing business (48%)

- Decreased consumer spending (29%)

- Affordable Care Act (28%)

- Shortage of qualified workers (18%)

- Domestic cost competition (15%)

- Credit availability (9%)

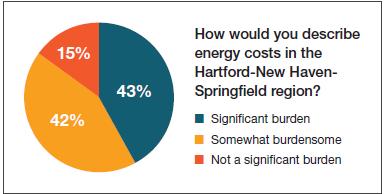

In a separate question, 85% of businesses characterized energy costs in the region as burdensome—half of those saying the costs are a significant burden.

Transportation

A 2013 CBIA survey found that Connecticut business leaders rank transportation in the top three areas—behind only economic development and education—for desired state government spending priorities.

Companies need to move goods and services with the speed and efficiency that allows them to compete in a global economy.

need to move goods and services with the speed and efficiency that allows them to compete in a global economy.

Well-maintained roads, safe bridges, and highways with good peak-hour volume-to-capacity ratios not only encourage economic development but also benefit workers, enhance a state’s quality of life, attract new busine

ss investment, and help create and sustain tens of thousands of construction-related jobs as well as jobs for planners, designers, and materials suppliers.

Earlier this year, Connecticut Gov. Dannel P. Malloy released a 30-year, $100 billion transportation plan for the sta

te that includes highway, bridge, and bus proposals. Massachusetts also recently identified priority projects to address road and bridge repairs, maintain airports, improve transit services, and ease congestion on the state’s major arteries.

Respondents to the 2015 Hartford-New Haven-Springfield Business Survey cited traffic congestion and poor infrastructure as the most pressing transportation issues for the region (67%), followed by lack of mass transit options (21%).

Nearly four out of five respondents use Bradley International Airport for business transportation, and a third use Bradley at least six times a year.

When asked what would increase their usage of Bradley, the number-one answer for all respondents was more direct flights (66%), followed by cheaper fares (48%) and more flights in general (24%). Seventy-eight percent said more flights from Bradley to Europe would benefit the region.

Respondents overwhelmingly agree that added commuter rail and better connectivity with Boston and New York would be a boon to the region.

Sixty percent say the planned intercity (New Haven-Hartford-Springfield) high-speed commuter rail will benefit the region, and 16% say it will benefit their business directly. Seventy-nine percent are in favor of a higher-speed commuter rail connecting New York, Boston, and points between.

More than 40% believe faster connections to Boston and New York would benefit their business, and 45% believe a commuter hub enhanced by train and bus service with nearby development would be attractive to workers.

Workforce

The Hartford-New Haven-Springfield region has the second most densely clustered concentration of colleges and universities in the country.

For the businesses we surveyed, this translates into an ability to recruit future workers (64% of businesses surveyed), hire interns (53%), train current employees (37%), gain access to expertise/consulting services (26%), technology transfer (18%), and R&D (15%).

When asked about the highest level of education for their new hires, more than half of respondents (53%) said most new employees had at least a four-year degree.

When asked about the highest level of education for their new hires, more than half of respondents (53%) said most new employees had at least a four-year degree.

Given the still tepid state of the economy and the amount of surplus labor in the marketplace (U-6 unemployment over 12%), it is somewhat surprising that 76% of respondents report having trouble finding and retaining qualified workers.

Fifty-eight percent say the main challenge is finding applicants with the necessary skills and education to do the job.

Businesses are most interested in employees with professional/soft skills, such as teamwork, leadership, punctuality, and work ethic (75% of respondents).

Also important are job-specific technical skills (59% of respondents); basic math, reading, writing, and problem-solving (51%); and advanced skills, e.g., scientific, computer, engineering (36%). All of these numbers are up from our last survey, in 2013.

The Internet (39% of respondents) and employee referrals (33%) are seen as the most effective tools for finding new employees. Only 14% of businesses surveyed are aware of InternHere.com, a free online service that matches college interns with prospective employers.

Employers largely offer their employees flexible schedules (73%), and a third allow telecommuting. In companies that offer it, workers telecommute anywhere between two to three times a month (34%), weekly (20%), two to three days a week (17%), and daily (12%).

Employers largely offer their employees flexible schedules (73%), and a third allow telecommuting. In companies that offer it, workers telecommute anywhere between two to three times a month (34%), weekly (20%), two to three days a week (17%), and daily (12%).

Sixty-one percent of respondents do not anticipate any retirements among their workers before the end of 2015. Over the next five years, however, over a third (34%) anticipate losing more than 10% of their workforce.

While a number of companies have leadership succession plans (42%), invest in job training (27%), are stepping up recruitment (24%), and are focusing on older worker retention (16%), 32% acknowledge they have done nothing to prepare for the upcoming wave of retirements.

Competition from Other States

Twenty-three percent of the businesses we surveyed have facilities outside the Hartford-New Haven-Springfield region, and in the past five years, 24% have been approached about relocating or expanding their business to other states.

Twenty-three percent of the businesses we surveyed have facilities outside the Hartford-New Haven-Springfield region, and in the past five years, 24% have been approached about relocating or expanding their business to other states.

The top five states trying to attract these businesses to their area are North Carolina (about half of the businesses contacted heard from this state, up from previous years), South Carolina (outreach by this state is up as well), New York (a new threat), Texas, and Florida.

Hartford-New Haven-Springfield businesses today are also more likely to consider relocating to other areas, with 37% pondering a move or expansion elsewhere (up from 31% in our last survey).

Among those, favored destinations are Florida, North Carolina, South Carolina, New Hampshire, and Texas.

These considerations take on greater significance given that quality of life is no longer the differentiator it once was, and Connecticut’s recent $2 billion tax hike has small businesses and large corporations alike exploring more business-friendly locations.

These considerations take on greater significance given that quality of life is no longer the differentiator it once was, and Connecticut’s recent $2 billion tax hike has small businesses and large corporations alike exploring more business-friendly locations.

Conclusion

Challenges remain as the Hartford-New Haven-Springfield region continues on a path toward full economic recovery.

Bright signs include businesses’ relative optimism about their own companies’ performance, a high concentration of educational assets, and plans for expansion and greater engagement in foreign trade.

Concerns persist, however, over business costs, workforce issues, transportation/infrastructure challenges, and aggressive recruitment efforts of other states. Concerns about tax hikes and labor shortages, in particular, are mounting.

The 2015 Hartford-New Haven-Springfield Business Survey was emailed in April and May 2015 to businesses in New England’s Knowledge Corridor—Hartford, Tolland, Middlesex, and New Haven counties in Connecticut, and Franklin, Hampden, and Hampshire counties in Massachusetts.

We received 408 responses, for a margin of error of +/–4.9%. More than two-thirds of respondents (69%) are based in Connecticut. Twenty-two percent are located in Massachusetts, and 9% are located in both states.

Most respondents have been in business longer than 10 years and employee up to 100 people.

The main industries represented are manufacturing (24%), professional services (23%), service (9%), and finance, insurance, and real estate (9%).

RELATED

EXPLORE BY CATEGORY

Stay Connected with CBIA News Digests

The latest news and information delivered directly to your inbox.

CBIA IS FIGHTING TO MAKE CONNECTICUT A TOP STATE FOR BUSINESS, JOBS, AND ECONOMIC GROWTH. A BETTER BUSINESS CLIMATE MEANS A BRIGHTER FUTURE FOR EVERYONE.