Federal Stimulus Bill Makes Proposed State Health Insurance Assessments Redundant

The Connecticut Insurance Department announced March 31 that the American Rescue Plan Act will increase affordability for healthcare plans offered on the state’s exchange and aid small businesses offering plans for their employees.

CID’s memo highlights the need to reassess the viability of the proposed assessments in SB 842 and HB 6447, two bills that assess commercial plans $50 million annually to provide subsidies to the state-run health insurance exchange.

However, the federal stimulus bill, highlighted below, will achieve a greater impact in reducing costs for individuals while not further raising the financial burden for commercial insureds.

The $1.9 trillion stimulus package signed into law by President Biden two weeks ago includes the biggest reform to health insurance since the passage of the Affordable Care Act in 2010.

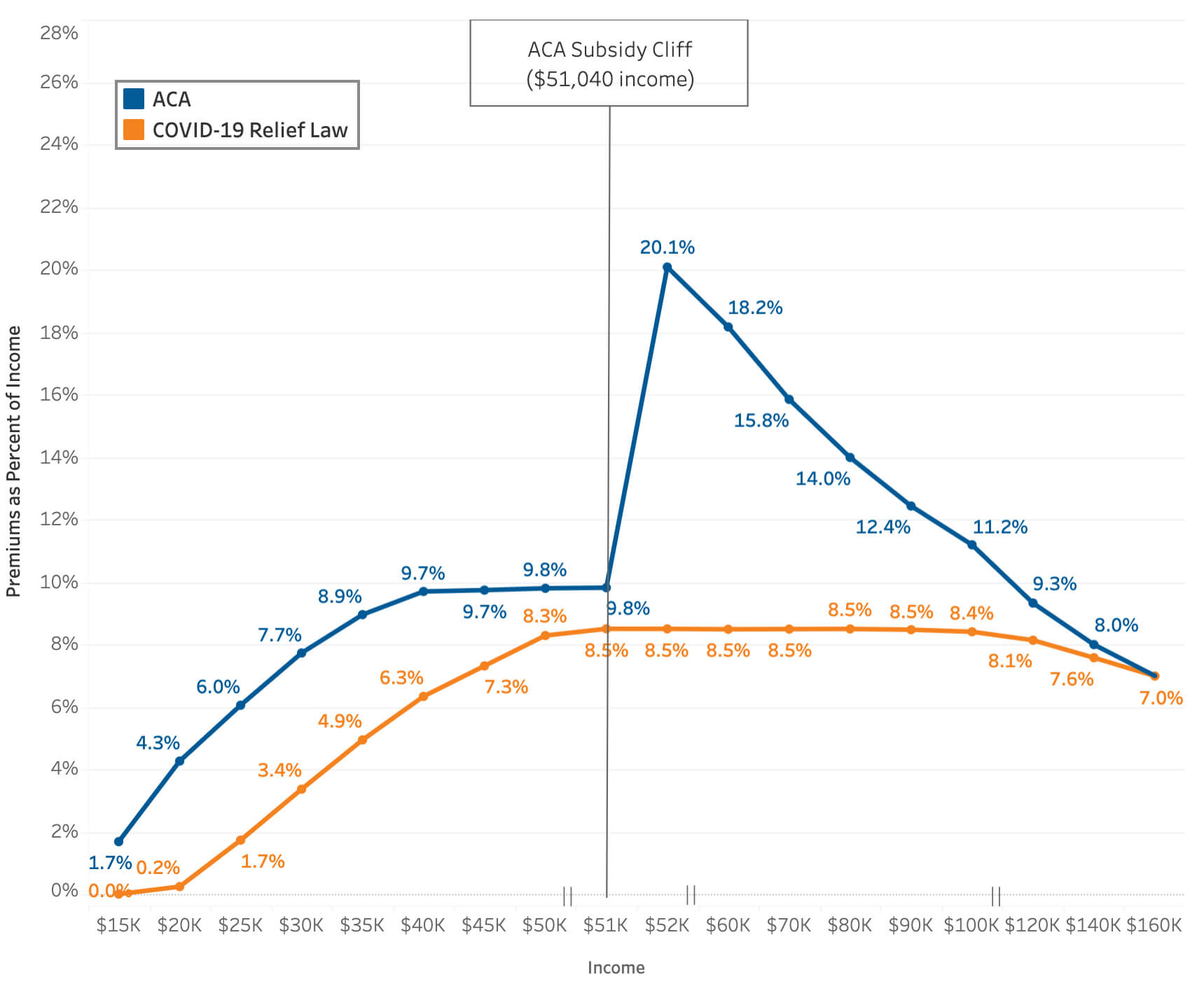

The package allocates more than $40 billion to the states that will increase premium tax credits and decrease the cost of insurance for millions of people across the country.

The plan extends eligibility for ACA subsidies for individuals and families with incomes over 400% of the federal poverty level and also increases subsidies for people at lower incomes who were already eligible under the ACA. These changes will expire in two years.

Positive Impact

This boost in subsidies will have a positive impact on individuals in Connecticut. According to the Department of Health and Human Services, 36,000 currently-uninsured individuals will now be eligible for tax credits.

Further, 4,700 individuals are now eligible for zero-dollar benchmark marketplace coverage.

According to the Kaiser Family Foundation, the number of people eligible for subsidies has increased 20% from 18.1 million to 21.8 million as a result of ARPA. The organization further projects that the average savings under ARPA will be $70 per month for current individual market purchasers.

The KFF projects ARPA will result in:

[A]n average savings of $213 (39% of current premiums after subsidies) per month for people with incomes between 400% and 600% of poverty to an average savings of $33 per month (100% of current post-subsidy premiums) for people with incomes under 150% of poverty (who will now have zero-dollar premiums for silver plans with significantly reduced out-of-pocket costs).

Take for example a 60-year-old individual who wants to purchase a benchmark silver plan. There’s a dramatic increase in subsidies available to that individual, with the existing subsidy cliff eliminated by a key reform in the bill that caps individual contributions to premiums at 8.5% of income.

COBRA

ARPA also includes substantial, temporary subsidies for COBRA premiums. The subsidy created by ARPA is equal to 100% of COBRA premiums for assistance eligible individuals, beginning the first day of the first month after the date of enactment of ARPA (April 1) and ending Sept. 30, 2021.

Assistance eligible individuals generally include those who were eligible for COBRA as a result of an involuntary termination of employment or a reduction in hours resulting in a loss of coverage, and who elected COBRA during the subsidy period.

The COBRA subsidy under ARPA will continue for assistance eligible individuals during the subsidy period.

Individuals who voluntarily terminate employment are not eligible for the subsidy.

The COBRA subsidy under ARPA will continue for assistance eligible individuals during the subsidy period, except in cases in which coverage terminates due to the assistance eligible individual becoming eligible for other health plan coverage, or the COBRA period (or maximum COBRA period) comes to an end.

Flexible Spending Accounts

ARPA also includes reforms that will benefit small businesses who provide health insurance to their employees.

The federal stimulus bill boosts the amount that small businesses can allow employees to put in dependent-care flexible spending accounts. For example, for married couples filing joint tax returns, the cap is increased from $5,000 to $10,500. For single filers, the cap is increased from $2,500 to $5,000.

Under the Consolidated Appropriations Act which passed in December, employees may roll over any unused funds if the company opts-in. Again, like the subsidies mentioned above, these rules are temporary.

With two bills pending for action in both the state House and the Senate that seek to assess commercial plans to provide subsidy relief for individuals seeking or currently enrolled in marketplace coverage, CBIA told lawmakers last month that the proposals serves a duplicative purpose due to ARPA.

Lawmakers would be well-advised to further study the impact of ARPA on marketplace affordability before inflicting any financial burden on commercial plans and their covered lives.

By all accounts up to this point, passing this $50 million assessment attempts to fix a problem that is already being addressed by ARPA.

For more information, contact CBIA’s Wyatt Bosworth (860.244.1155) | @WyattBosworthCT.

RELATED

EXPLORE BY CATEGORY

Stay Connected with CBIA News Digests

The latest news and information delivered directly to your inbox.

CBIA IS FIGHTING TO MAKE CONNECTICUT A TOP STATE FOR BUSINESS, JOBS, AND ECONOMIC GROWTH. A BETTER BUSINESS CLIMATE MEANS A BRIGHTER FUTURE FOR EVERYONE.