Unemployment Trust Fund Reforms Restore Solvency at No Cost to State

Connecticut employers are again urging lawmakers to shore up one of the most vital safety nets workers have: the state’s Unemployment Trust Fund.

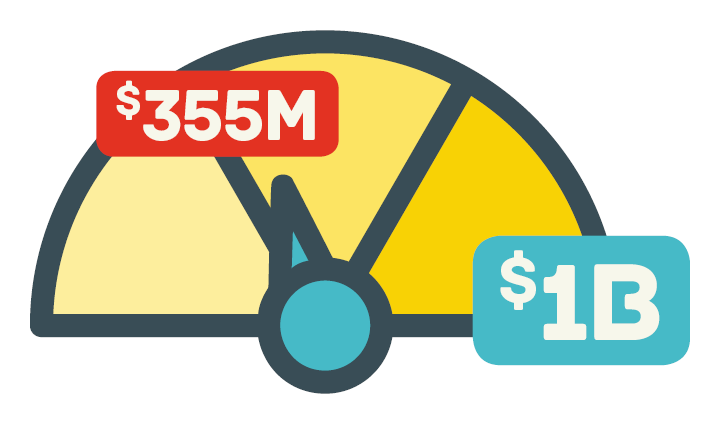

As of January 2018, the fund’s balance was $383.8 million—less than 40% of state’s $1 billion solvency goal.

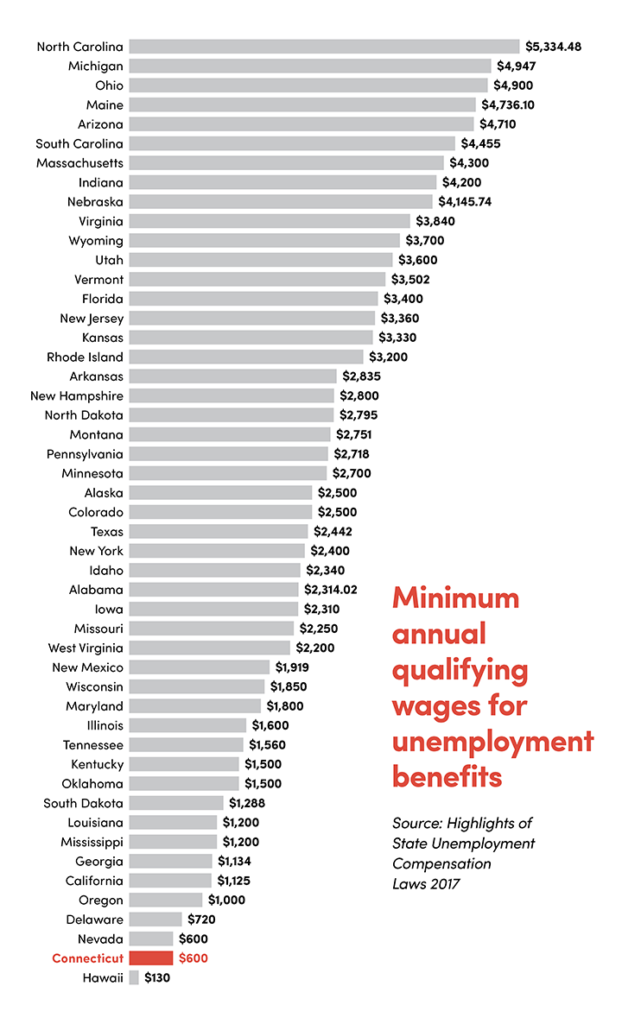

Connecticuit’s qualifying threshold for unemployment benefits hasn’t changed in 50 years and is the second lowest in the U.S.

CBIA’s Eric Gjede will testify March 13 before the legislature’s Labor and Public Employees Committee in support of the bill, calling its reforms a “do no harm approach” to restoring the fund’s solvency.

The 2008-2010 recession decimated Connecticut’s workforce, forcing the state to borrow nearly $1 billion from the federal government to shore up the fund so thousands of laid-off workers could collect unemployment benefits.

The business community was solely responsible for that debt, and repaying the loan caused the per-employee unemployment tax on Connecticut employers to more than quadruple from $42 to $189.

The money has since been paid back and the tax rescinded. But Connecticut must restore the fund to ensure the need to borrow never happens again.

Neighboring states endured the same recession, yet they were able to restore solvency to their trust funds far quicker than Connecticut.

“The reason is that they have adopted unemployment benefit reforms to curtail waste and abuse that Connecticut has long refused to adopt,” Gjede said.

Common-Sense Reforms

These commonsense reforms can be found in HB 5480:

- Raising the minimum earnings to qualify for unemployment benefits to $2,000. Claimants in Connecticut need only earn $600 in a year to qualify for benefits—the third-lowest earnings requirement in the U.S. For perspective, 32 states/territories require between $2,000 and $5,000 in earnings. Connecticut hasn’t raised its earnings requirement in 50 years.

- Prohibiting claimants from receiving unemployment benefits until they have exhausted their severance pay. According to the state Department of Labor, this delay saves the fund up to $57 million a year.

Connecticut must follow other states' lead on unemployment reforms if we are serious about preserving benefits for future workers.

- Freezing the maximum weekly benefit rate in any year in which we have not attained 70% of our trust fund solvency goal. The maximum benefit rate increases by up to $18 every year and rose throughout the recession. Foregoing increases in years when the fund is unhealthy prevents the problem from getting worse. This saves approximately $1.6 million per year and won't result in benefits being cut from current levels.

- Redefining "one instance" of unexcused employee absence from work to mean a single day of no call, no show to work. Current law defines one instance as "one day or two consecutive days." Employers commonly misinterpret this rule and end up having to pay unemployment benefits for employees who abandoned their job or stopped showing up.

Avoid Job-Killing Tax Hikes

Gjede urged passage of HB 5480 because it restores solvency to the fund, avoids benefit reduction for most workers, and doesn't have any job-killing tax increases.

"Connecticut needs to follow other states' lead on unemployment benefit reform if we are serious about preserving our Unemployment Trust Fund for future workers," he said.

"Adopting these reforms will help return solvency to our Unemployment Trust Fund and prevent heavy borrowing from the federal government during future recessionary periods."

For more information, contact CBIA's Eric Gjede (860.480.1784) | @egjede

RELATED

EXPLORE BY CATEGORY

Stay Connected with CBIA News Digests

The latest news and information delivered directly to your inbox.

CBIA IS FIGHTING TO MAKE CONNECTICUT A TOP STATE FOR BUSINESS, JOBS, AND ECONOMIC GROWTH. A BETTER BUSINESS CLIMATE MEANS A BRIGHTER FUTURE FOR EVERYONE.