OFA Says Reforms Restore Unemployment Fund’s Solvency

An analysis by the General Assembly’s nonpartisan Office of Fiscal Analysis shows a bill designed to restore solvency to the state’s Unemployment Compensation Trust Fund does just that.

OFA determined HB 5480—by fixing shortfalls in the fund—could prevent the state from having to borrow hundreds of millions of dollars from the federal government during the next recession.

The state’s Unemployment Compensation Trust Fund is about $900 million short of its solvency goal.

“Unemployment is low in Connecticut, which makes this the perfect time for the legislature to focus on shoring up the fund,” said CBIA’s Eric Gjede.

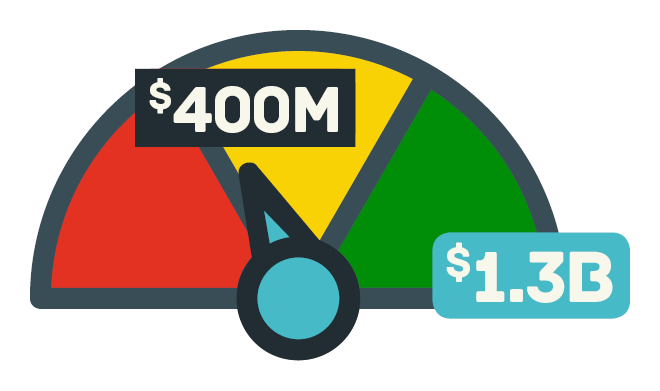

“Although the fund’s current balance continues to hover around $400 million, that is far short of its $1.3 billion solvency goal.”

$1 Billion Federal Loan

Gjede noted that prior to the last recession, the state was nowhere close to the solvency goal.

Then, when the recession hit and Connecticut companies were forced to lay off tens of thousands of workers, there wasn’t enough money in the fund to pay unemployment benefits.

That caused the state to borrow nearly $1 billion from the federal government to shore up the fund so these workers could collect unemployment benefits.

But the cost of paying that loan back—with interest—fell on Connecticut employers, who saw their federal per-employee unemployment tax more than quadruple from $42 to $189 per employee.

The loan has since been paid off, but the state has yet to take the necessary steps to ensure the fund’s solvency and negate the need to borrow again during another economic downturn.

Specific Reforms

HB 5480 takes several specific steps to stabilize and fortify the fund, including:

- Raising the minimum earnings to qualify for unemployment benefits to $2,000. Claimants in Connecticut need only earn $600 in a year to qualify for benefits—the third-lowest earnings requirement in the U.S. For perspective, 32 states or territories require between $2,000 and $5,000 in earnings. Connecticut hasn’t raised its requirement in 50 years.

- Prohibiting claimants from receiving unemployment benefits until they have exhausted their severance pay.

- Freezing the maximum weekly benefit rate in any year in which we have not attained 70% of our trust fund solvency goal. The maximum benefit rate increases by up to $18 every year and rose throughout the recession. Foregoing increases in years when the fund is unhealthy prevents the problem from getting worse.

- Redefining “one instance” of unexcused employee absence from work to mean a single day of no call, no show to work. Current law defines one instance as “one day or two consecutive days.” Employers commonly misinterpret this rule and end up paying benefits for employees who abandoned their job.

Amid chronic state budget troubles, lawmakers should jump at the opportunity to take preventative action on this simple, direct proposal.

But they also noted this cost will come from the fund, where the savings in the first year alone more than makes up for it. In addition, the savings to the state and municipalities further outweigh any cost.

Preserves Safety Net

Despite all the good this bill does to ensure future workers have unemployment benefits, progressive advocates oppose the measure, claiming it balances the fund on the backs of workers.

That, however, is a tough argument to make given that workers don't contribute a penny to the fund, and Connecticut unemployment benefits continue to be among the highest in the nation.

HB 5480 yields massive savings for an important safety net while carefully avoiding a reduction in benefits to workers the program was intended to protect.

Yet some lawmakers are so ideologically opposed to what they see as a perceived reduction in benefits, that this bill faces an uncertain future.

Amid chronic state budget troubles, lawmakers should be jumping at the opportunity to take preventative action on this simple, direct proposal.

Corrective action, after the fact, always comes with a heavier price.

For more information, contact CBIA's Eric Gjede (860.480.1784) | @egjede

RELATED

EXPLORE BY CATEGORY

Stay Connected with CBIA News Digests

The latest news and information delivered directly to your inbox.

CBIA IS FIGHTING TO MAKE CONNECTICUT A TOP STATE FOR BUSINESS, JOBS, AND ECONOMIC GROWTH. A BETTER BUSINESS CLIMATE MEANS A BRIGHTER FUTURE FOR EVERYONE.